Food Tech & Media Landscape 2019

Brita Rosenheim has been tracking the food tech ecosystem for the past decade. Along the way, we have seen many business models and fads come and go, from daily deals and local loyalty schemes, to meal kits and the on-demand convenience economy, to the ever elusive promise of personalization via some version of “Pandora for Food”.

Reflecting on the profound changes and growth that have occurred within the ecosystem over that time frame, I’ve decided to make significant adjustments to the annual Food Tech & Media Landscape to reflect today’s new realities. In the most recent year we have seen previously hot sectors cool (like e-commerce meal delivery and guided cooking); new sectors take shape (like personalized nutrition and voice-driven platforms); and many B2B platforms that are leading to, among other things, new cross-sector “enabling technology” plays.

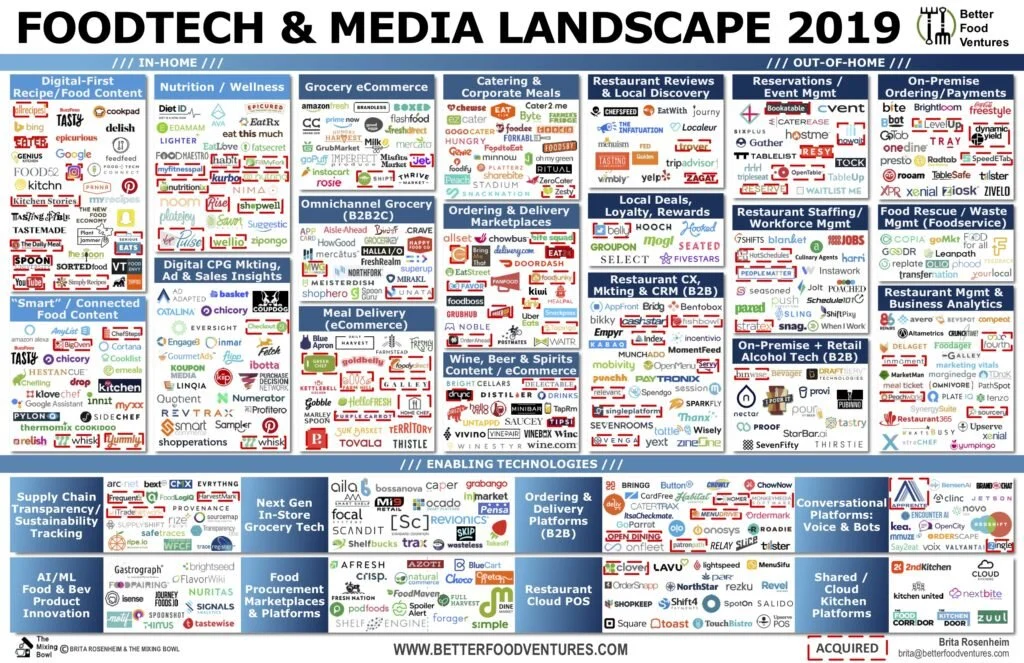

Landscape Map Background

This is a heatmap, not a comprehensive catalog: While clearly not exhaustive, this map is meant to illustrate the layers and variety of technology solutions, early stage to mature, both consumer-facing and B2B technologies. Food tech is a tremendous global opportunity, however in order to narrow the perspective (and eyestrain!) I have only included technologies with a US customer/user-base.

“Food Tech” here means food distribution through end consumption:Depending on which hat you wear, and where you sit within the ecosystem, “Food Tech” can mean many things. Whereas my colleague Seana Day publishes an AgTech Landscape, which maps seed through supply chain technologies, this landscape meets her in the “Messy Middle” with traceability/sustainability platforms, and then moves further downstream to food/bev product innovation, media, marketing, and the many varied paths towards end consumption.

Focus is on IT-driven, primarily VC-funded technologies:While VC funding is not a requirement to scale, it is often an enabler of growth, and this Landscape primarily highlights innovative startups and higher-growth companies that are enabling the food ecosystem via technology. Which means, although still part of the Landscape’s title and framework, there is a significant decrease of media categories versus previous versions of the map, reflecting the broader shift and struggles of the media industry with few avenues for content monetization. Separately, given that food ecommerce is no longer niche and is now integral to the strategy of most brands, the ecommerce lens has been shifted to focus on technology solutions and platforms within fresh/grocery and meal delivery.

The new doubledecker format helps to simultaneously frame the evolution of the consumer consumption journey from in-home to out-of-home, while also highlighting enabling B2B technologies that span multiple sectors and/or categories: The top portion of the Landscape is organized left to right by a customer’s final location of engagement/consumption in an effort to categorize the variety of technology and media players shaping how consumers discover, cook, order, consume, and enjoy food experiences today. The horizontal band at the bottom breaks out a number of “Enabling Technologies”, recognizing that a growing number of B2B food tech companies are connecting multiple partners to create a more robust food system.

Hardware is (mostly) unplugged from this landscape: You will note this Landscape does not carve out dedicated categories focused on robotics, automation and IoT devices, despite the recent momentum. This is intentional, as the increasingly crowded food-related hardware space warrants its own dizzying landscape analysis. For example, The Spoon recently created a thoughtful Food Robotics Market Map that addresses a number of hardware-driven sectors. I will say that, in general, many of the VC-backed hardware devices have not really scaled to success and we should expect more downround financings, consolidations and acquisitions in the near term.]

And now, onto my thoughts and analysis on the recent shifts in the food tech ecosystem.

Key Takeaways

IS CONNECTED CONTENT PANNING OUT?

Alongside next-gen IoT cooking innovations, over the past couple of years we have seen a number of tech-savvy recipe content publishers leveraging technology platforms in order to transform content into guided and conversational cooking offerings.

However, despite the tremendous breakthroughs entrepreneurs have made to augment an in-home cooking experience that is more convenient, enjoyable, personalized or nutritious, this “connected content” category has largely remained in the “nice to have” business model stage (versus “need to have”). To date, neither corporations nor consumers have been willing to foot the bill for recurring revenue around additional capabilities and insights.

As of yet, the connected kitchen ecosystem that was supposed to be a bridge to new business models like product/content subscriptions, ecommerce, advertising or SaaS data plays, has simply not yet panned out the way most entrepreneurs had hoped.

While everyone believes there is value in the data from smart devices, to date not many have been willing to pay for it. That said, a recent announcement by Discovery (via The Food Network) and Amazon (via Alexa) shows that the dream is still alive, as the two companies plan to launch a live action subscription service (at $7/month) to provide cooking instructions, recipes and connected grocery services (via Amazon, Instacart and Peapod) in select markets this October.

‘PERSONALIZED NUTRITION’ SHOULDN’T REQUIRE PRECISION OUTCOMES

While “personalized nutrition” is a big buzzword these days with CPGs (including Mars, Kraft Heinz, and Nestle) using the term to boost their innovation cred, a bulk of the funding and acquisition activity in the space has actually been around nutraceutical/vitamin companies (likely due to healthy ecommerce recurring revenue models) rather than diet/food-driven technology platforms.

One issue which has hindered many startups in this category is that there are currently few straightforward business models outside of ecommerce or subscriptions, and retention has proved to be quite challenging. The B2B SaaS market has recently begun to develop and remains promising, however to date, many of the technology platforms, whether direct to consumer or B2B, just haven’t scaled.

Beyond business model challenges, I believe a key issue within this sector is that many companies are trying to personalize with the goal of chasing a precision outcome that is just not possible. Normalized human behavior, especially when it comes to food, is simply not precise. Many companies have built technologies that require 1) an engaged user base, 2) active tracking of specific food/health behavior, and/or 3) accurate self-reporting – which, respectfully, are often fleeting, imprecise and inaccurate.

There are absolutely times that a prescriptive approach is helpful in order to keep health goals on track, or to manage chronic illnesses, but much like the many, many (many) “Pandora for food” concepts I have seen over the past 10 years – all of which promised to tell me precisely which recipe, dish, restaurant, drink or product I would undoubtedly love – I believe it is a mistake to build upon the premise that there is one (or few) right answers, when in reality, there are countless iterations of success.

Thus, the next generation of personalized nutrition platforms should 1) be versatile, adaptable and seamless enough to only warrant passive engagement; nudging the consumer towards healthier decisions, 2) re-envision how to minimize inputs (if any) of food/health behavior (outside of on-boarding and updates), and 3) eliminate the need for self-reporting.

On this front, in the near term, we are seeing an uptick of momentum in B2B platforms that are setting a data foundation and/or nutritional lens in order to enable various players throughout the food ecosystem to provide enhanced and personalized health experiences. For example, Diet ID has partnered with SunBasket to gather insights on customers’ dietary patterns and seamlessly help recommend meals that align with their goals. Edamam recently partnered with restaurant/catering companies like Juice Generation and ZeroCater to easily integrate nutrition and dietary info across all menus and dishes. Lighter Nutrition, has recently partnered with Mass General Hospital (among others) to provide an enterprise platform for health care providers to be able to customize meal plans and grocery shopping for their patients.

As I mentioned during a talk at Groceryshop 2019, I think food retailers/grocers are in a particularly unique position to impact healthy choices. Wellness is a clear strategy as grocers look to differentiate in an increasingly commoditized sector, and thus while the national chains have more budget for these initiatives, it is all the more important for small/midsize grocers to compete. Regional grocer Heinen’s is ahead of the game, as they hired a chief medical officer and chief dietitian years ago, but they recently kicked it up a notch with the recent announcement highlighting their own Fx platform for personalized diet plans. For grocers without their own chief medical officer, there are startups like FoodMaestro and Spoon Guru, which partner with grocers to layer health data into the shopping experience.

In summary, the personalized nutrition technology space shows huge potential in the long-run and while it is showing some momentum in the short-term, there are still fundamental challenges to “personalized nutrition” platforms that will likely take this sector more time to mature.

VOICE AND BOTS OFFER A NEW AVENUE OF ENGAGEMENT

Restaurants, brands, retailers and advertisers have increasingly started to think in terms of conversations (rather than one-time transactions or ad placements) in order to maintain consumer engagement and engender lifetime value.

In addition to McDonald’s recent acquisition of drive thru AI-voice platform, Apprente, the last couple of years have been witness to a surge of AI-driven conversational platforms for the food industry. From automated brand communication to voice-driven platforms focused on nutrition, grocery, coffee, online ordering, drive thrus, and even Back-of-House solutions focused on restaurant bar inventory, there are numerous use cases to ditch the typing (or phone, pen and paper!) and streamline via conversational technologies.

THE PRIMACY OF FIRST-PARTY DATA: DATA ANALYTICS COMPANIES ARE GETTING BOUGHT BY THEIR WOULD-BE CLIENTS

Counter to the more traditional network effect approach where clients of software companies benefit from leveraging their data by blending it with that of their competitors, an interesting recent trend has emerged where a handful of early stage AI-and data-analytics startups within the food, retail and restaurant sectors were acquired early on by a customer in order to bring data and insights in-house.

This highlights the ever increasing primacy of first-party data as a competitive differentiator. Recent examples include McDonald’s purchases of Dynamic Yield, Walmart’s acquisition of Aspectiva and even Instacart’s acquisition of MightySignal.

THE CONVERGENCE OF “OMNI-CHANNEL MEALS”

There has been an overall convergence of in-home food channels that one might call “omni-channel” consumer food delivery as consumers are making less of a distinction between delivery of groceries, prepared meals, meal kits, e-commerce CPG purchases and restaurant delivery.

When Amazon acquired Whole Foods two years ago, I hypothesized that the Amazon/Whole Foods combination would be a threat to both brands and local restaurants. I believed that the competition from a more streamlined grocery category capable of delivering its own in-store prepared food, private branded products and meal kits ( a “grocerant” platform) combined with Amazon’s logistics, would be a threat to local restaurants. However, to date, it has not played out that way – which in part shows how hard it really is to execute on a successful food program.

PRIVATE EQUITY’S GAZE SHIFTS FROM RESTAURANTS TO RESTAURANT TECH

As private equity activity continues to sizzle in the restaurant sector, we are seeing private equity players begin to enter the restaurant tech category via rollups and mergers of incumbents. That said, while you would think some of these investors are looking for synergies or operational efficiencies among their restaurant portfolio, there is actually little overlap between the restaurant and restaurant tech private equity investors stepping into the space (save for Danny Meyer’s Enlightened Hospitality).

Some recent private equity entrants to the space include Marlin’s merger of Fourth and HotSchedules, Vista Equity Partners and Enlightened Hospitality Investments cash infusion into Gather, and Great Hill’s $65 million investment into Paytronix last year.

The food tech and restaurant tech sectors haven’t quite caught up to the broader financing ecosystem, however, as Pitchbook notes that PE-led acquisitions accounted for almost 40% of North American M&A volume in 1H 2019 (up from a historical average of <30%).

RESTAURANT DELIVERY CONTINUES USING “GO BIG OR GO HOME” PLAYBOOK

We continue to see a huge wave of continued consolidation in regional restaurant delivery networks as the national players need to keep scaling in order to lower per- customer costs in the technology, marketing, infrastructure and customer support realms. Nationally, Caviar’s recent $410 million acquisition by DoorDash was notable given there were no buyers when it was being shopped three years ago (reportedly they were asking for $100 million), but fast forward to 2019 and Square was able to sell it for a significant premium.

Softbank, a major investor in DoorDash, is famously known to be a believer in the market-grab (i.e. “go big or go home”) philosophy and likely used that as justification for paying the premium over Square’s acquisition price. It is questionable whether Caviar’s business performance alone could have justified paying that premium. Time will tell whether the combination of DoorDash and Caviar will provide enough market momentum to get both companies to stop bleeding cash.

FOOD TECH SERVES LUNCH FOR CORPORATES

The convenience economy is no passing fad. And while we have seen many food delivery companies unable to “go big” already “go home” through shutdowns and firesales, it has also paved the way for new, and capital efficient approaches to personalized food distribution. Within this, corporate meals have been a particularly bright spot.

The fundamental challenge of most food delivery companies has been to make the economics work to deliver one meal to one person/family across different places and times. In contrast, as the entrepreneurs behind the 40+ venture-funded corporate lunch startups have figured out, group dining can actually deliver profitable margins. As such, there have been new crops of competitors entering the fray on a regular basis; 35% of these VC-funded concepts were founded in only the past 5 years.

But as we discussed on the “Future of Corporate Lunch” panel at SKS 2018, there are actually a plethora of tech-enabled competitors vying for the business opportunity of the lunchtime worker – ranging from quick service brands like Sweetgreen, who is using the recent cash infusion to support corporate delivery platform Outpost, to last mile delivery services from restaurants and dark kitchens, to pre-made meal solutions from retailers, grocers and D2C ecommerce players. And don’t rule out in-office smart vending, IoT, robots, or of course, the incumbent institutional dining providers.

As an aside, the same volume-driven economic motivator is also bolstering an increased focus on college towns and campuses, especially since they can deliver population density outside of major markets. Besides college food marketplace Tapingo, which was acquired by Grubhub in 2018 $150 million, you will find a number of other college-focused food platforms in the Landscape including Kiwi Campus, Snackpass, and Hooked. Even Sally the salad-making robot is heading off to college!

While the economics of corporate lunch delivery can be solid, we have not yet seen even the beginning of the national rollups in this space. As most corporate and catering startups are still regional (even if the regions are large or span multiple parts of the country), I predict this will be a compelling area of consolidation in short time.

WITH THIRD-PARTY TECH “PARTNERS” LIKE THESE DO RESTAURANTS NEED ENEMIES?

As we initially discussed in our 2018 Restaurant Tech Ecosystem report, it’s tough to be a restaurant or hospitality operator today. We’ve increasingly seen a myriad of issues cannibalizing operators’ margins, including rising rents and labor costs, as well as the onslaught of third-party ordering/delivery services. And simultaneously, operators are being bombarded by a nonstop offering of emerging technologies which are promising front-of-house (FOH) and back-on-house (BOH) efficiencies.

Currently, one of the most talked about threats to restaurants’ income statements are from third-party ordering/delivery technology “partners” that are skimming significant margins from restaurant operators for off-premise orders (both take-out and delivery).

These third-party marketplace partners are selling restaurants the chance to increase reach and volume through delivery and larger platforms, arguing that the additional incremental sales volume is pure margin due to significant fixed costs in the restaurant model. But that lens is too simplistic, as off-premise sales include additional indirect and hard to measure costs, and many operators are actually reporting negative margins on third-party delivery (“3PD”). For more depth on this topic you should read the medium post by the CEO of customer engagement platform Thanx, in his comprehensive takedown on the massive disruption facing restaurants today.

Beyond P&L implications, there is also a data gap with many third-party marketplaces, as many of these partners are looking to capture the customer data for their own platform’s success. When they are unwilling to share even basic data on the restaurant’s own customers, the 3PDs are showing their hand in that they view these restaurant customers as their own customer base.

THE BIFURCATION OF RESTAURANT CUSTOMER LOYALTY: THIRD-PARTY ORDERING/DELIVERY MARKETPLACES ARE POISED TO TAKE OVER AS UNIVERSAL LOYALTY PLATFORMS

One of the early trends I tracked in local tech was the digital reinvention of the punch/stamp loyalty card – with startups promising one universal loyalty account to replace them all, by using gamification, check-ins, push notifications, digital wallets and the lure of a network of deals at a consumer’s fingertips.

Many startups built a business plan around becoming the universal loyalty network, spending time (and capital) to build a consumer-facing brand in order to simultaneously woo local merchants with their impressive user base. In years past this was an overflowing category in the Landscape, however the logos have dramatically slimmed as most of those startups have since either been acqui-hired, pivoted out of the food/restaurant sector or simply failed. Escaping the deadpool, Fivestars is a notable exception, having continued to successfully scale via numerous merchant verticals and geographies.

That doesn’t mean loyalty schemes have disappeared, in fact, white label (i.e. merchant-branded, not tech-company-branded) solutions are thriving, and you will see that the Landscape category focused on B2B restaurant solutions for CX (Customer Experience), Marketing and CRM (Customer Relationship Management) is bursting at the seams. I predict this category will continue to grow in next year’s iteration of the Landscape.

A key reason for the struggles of the first crop of loyalty startups was that a many of the founders and technologists lacked local merchant/restaurant experience, and struggled to create compelling win-win solutions as they tried to solve for the operational complexities related to running a long-tail, two-sided marketplace. It is a hard business to scale, and ultimately, without the network effect, the value exchange was simply not compelling enough for users (or merchants) to remain engaged.

However, there is another lesson to be learned here that can be applied to how we think about the third-party ordering/delivery scene. Many of the loyalty startups were ultimately competing against their own customers (the merchants) for branding and mind share, which by default did not create a win-win model to best serve the interests and priorities of restaurants/merchants. This tension is again showing up with third-party ordering/delivery marketplaces, but rather than just competing for mind share, the leading third-party partners seem to be increasingly setting their sights on owning the customer’s entire journey. Grubhub’s recent launch of a loyalty program supports this thesis.

In a relatively short time, due to the ease, variety and scale offered via marketplace apps, the customer’s loyalty journey has transformed, now bifurcating to either: 1) direct ordering from the restaurant (online or in-person), or 2) loyalty to one or many ordering/delivery platforms. Thus the future success of many restaurants depends on handing power back to the operators, which is why there is such a healthy market for white-label ordering & delivery, and automated customer engagement platforms.

Looking Ahead

I’ve enjoyed watching the Food Tech sector grow over the last decade, but am certain we will see even more meaningful growth in the decade to come. At Better Food Ventures, we believe technology will prove to be the single biggest catalyst to solving critical problems across the global food ecosystem, and we are particularly encouraged by the continued growth of tech-driven innovations and frameworks across the food sector.

The Food Tech & Media Landscape will continue to change as the industry matures, and as such, we depend on the wisdom of the participants in the space. I welcome your thoughts and reactions and look forward to following this sector together in the coming years.

This post was originally published by Brita Rosenheim at The Spoon.